Improving the characterization of the distribution of extreme values is of paramount importance.-- Alan Greenspan, former Fed chair

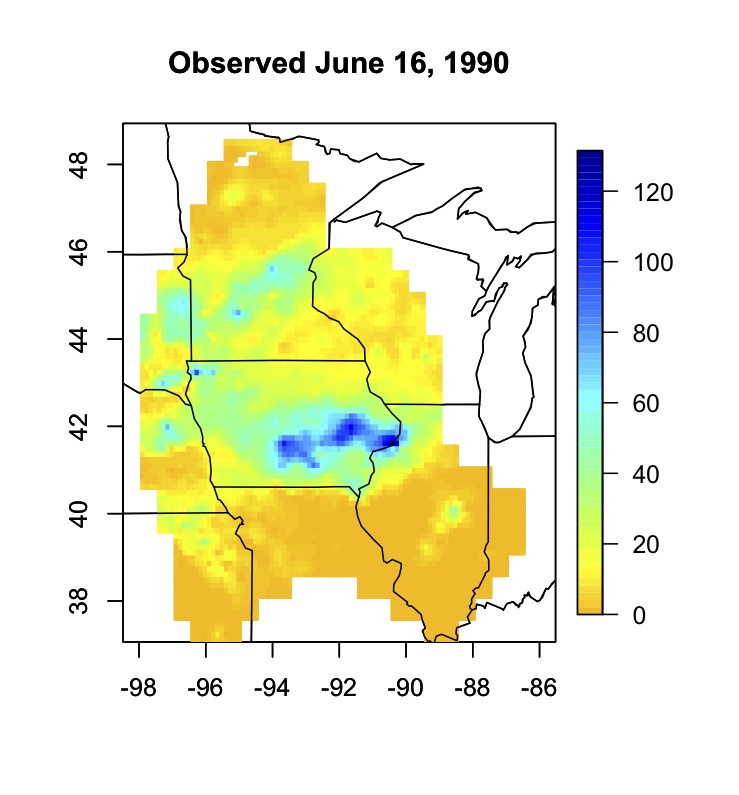

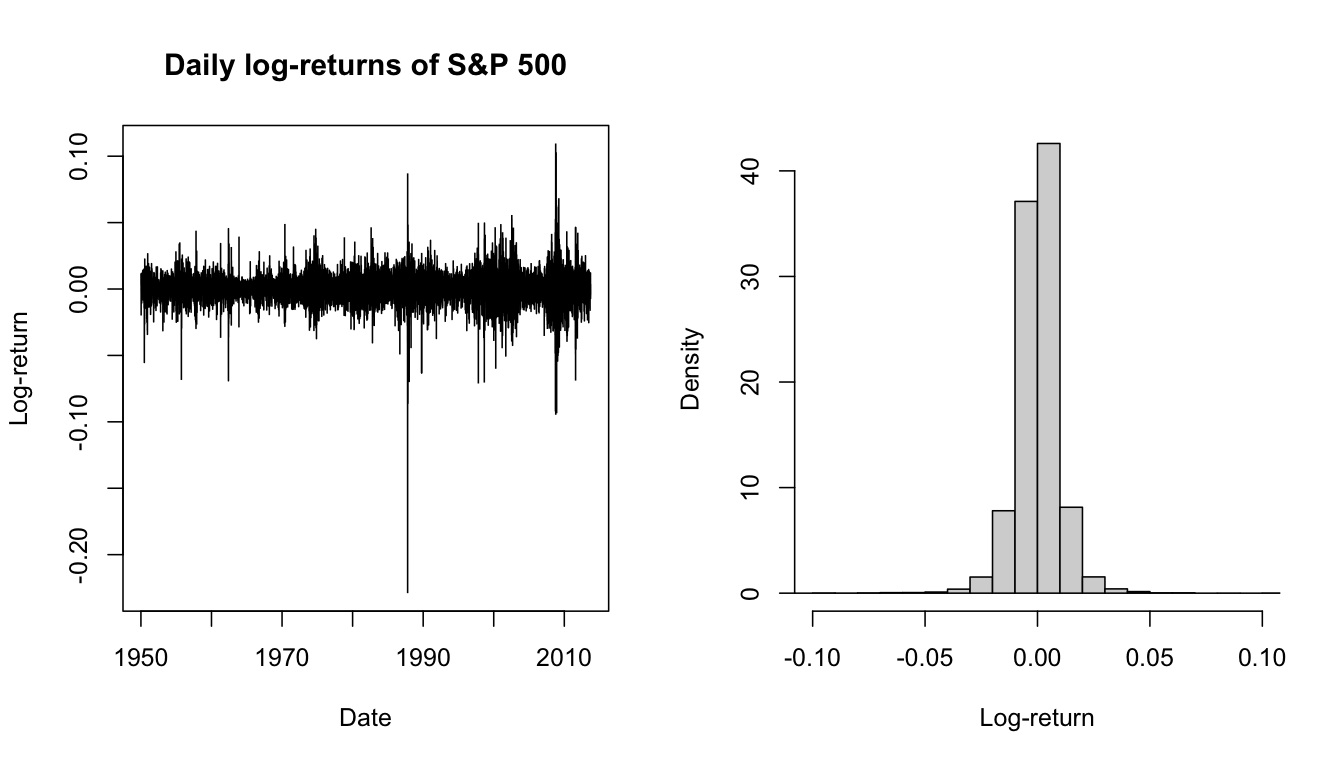

My primary personal research interests lie in the field of extreme value theory (EVT), the branch of probability and statistics which aims to describe and model tail events and their associated risks. While the probability theory underlying the study of extremes has been well-developed for decades, the suite of statistical methodology for the modeling of extreme values is currently growing rapidly. I have primarily worked on the modeling of multivariate extremes; to give an example, one may wish to estimate the probability of multiple securities in a financial portfolio experiencing tail loss events (of magnitude previously unseen) simultaneously. EVT provides tools to perform such an estimation given observed data. My entry into the field was through the study of climate extremes, and I published research in both the statistical and climate science literature on this topic. I have also worked on extreme value problems in financial risk management.

My primary personal research interests lie in the field of extreme value theory (EVT), the branch of probability and statistics which aims to describe and model tail events and their associated risks. While the probability theory underlying the study of extremes has been well-developed for decades, the suite of statistical methodology for the modeling of extreme values is currently growing rapidly. I have primarily worked on the modeling of multivariate extremes; to give an example, one may wish to estimate the probability of multiple securities in a financial portfolio experiencing tail loss events (of magnitude previously unseen) simultaneously. EVT provides tools to perform such an estimation given observed data. My entry into the field was through the study of climate extremes, and I published research in both the statistical and climate science literature on this topic. I have also worked on extreme value problems in financial risk management.

My work in applications of statistical methodology spans a wide range of fields, including climate science, astrophysics, finance, and environmental monitoring. In my current position, I work on applied problems in healthcare, engineering, and technology, using modern statistical and machine learning methods for dimension reduction, time series forecasting, and network analysis. I am also interested in the development of novel methodology for analysis of multivariate extreme events; as part of my dissertation, I proposed an estimation scheme for a phenomenon known as hidden regular variation.

Below is a partial list of publications and presentations. For a full list and more detail, please see my current CV.

Publications and Manuscripts

Work in preparation

Presentations

Joint Statistical Meetings, Chicago, IL. August 1, 2016.

International Society for Clinical Biostatistics 2015 Conference, Utrecht, Netherlands. August 26, 2015. slides (pdf)

Joint Statistical Meetings, Seattle, WA. August 13, 2015.

Department of Statistics Environmental Seminar, North Carolina State University (Invited), Raleigh, NC. March 3, 2015. slides (pdf)

Department of Statistics Seminar, Columbia University (Invited), New York, NY. April 14, 2014. slides (pdf)

SIAM 2014 Conference on Uncertainty Quantification, Savannah, GA. March 31, 2014.

Department of Statistics Seminar, University of Wisconsin-Madison, Madison, WI. September 23, 2013.

Joint Mathematics Meetings, Baltimore, MD. January 17, 2014.

Eighth International Conference on Extreme Value Analysis (Invited), Shanghai, China. July 11, 2013.

Department of Statistics Seminar, Carnegie Mellon University, Pittsburgh, PA. January 28, 2013.

Department of Statistics Colloquium, University of Missouri, Columbia, MO. January 24, 2013.

American Geophysical Union 2013 Fall Meeting, San Francisco, CA, December 12, 2013.

Department of Meteorology Colloquium, Pennsylvania State University, State College, PA, October 2, 2013.

Applied Probability and Statistics Seminar, University of St. Thomas, St. Paul, MN, December 6, 2013.

Concordia College Mae Anderson Alumni Lectures (Invited), Moorhead, MN. January 20, 2012. slides